Community Pharmacy Is Changing

Why Wellness Clinics Could Be Part of the Next Opportunity

The UK community pharmacy sector is under pressure, but it is also changing quickly. The Pharmacy Show 2026 report, An Overview of the UK Community Pharmacy Landscape 2026, points to a sector moving away from a purely dispensing-led model and towards a more service-led, clinically focused and commercially resilient future.

For the CTA, this shift matters. Community pharmacies are already trusted healthcare access points. They sit within local communities, see patients regularly, and are increasingly expected to do more than dispense prescriptions.

As pharmacies look for new income streams, better use of clinical skills and stronger patient relationships, pharmacy-based wellness clinics could become an important part of the next model of care. That may include lawful medical cannabis pathways where appropriate, but only where they are properly governed, clearly defined and supported by the right clinical oversight.

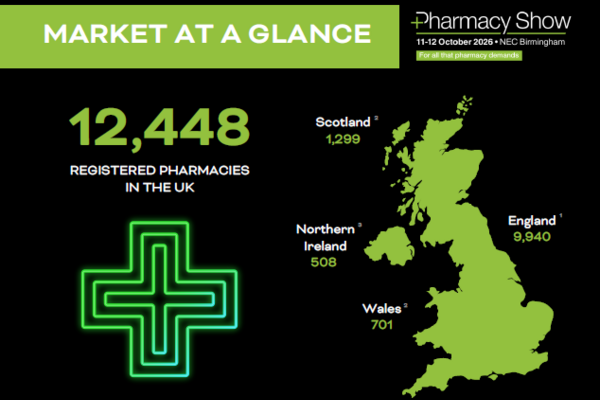

The report identifies 12,448 registered pharmacies across the UK, supported by a workforce of 95,613 pharmacy professionals. England accounts for 9,940 registered pharmacies, with Scotland at 1,299, Wales at 701 and Northern Ireland at 508. The report also identifies 454 online pharmacies.

This is a substantial healthcare network, but it is operating under sustained pressure. Community pharmacy is facing funding constraints, rising operating costs, workforce shortages, medicines supply issues and growing prescription demand.

By the end of April 2026, community pharmacy numbers in England had fallen by 44 year on year and by 897 compared with January 2021. The report points to inadequate funding, rising costs, and recruitment and retention difficulties as reported drivers of closures.

For pharmacy owners, this is not simply a difficult trading period. It is a structural challenge. The traditional model is being tested, and many pharmacies need practical ways to build resilience for the future.

One of the clearest findings in the report is the shift in ownership. In England, small independents owning one to five pharmacies now represent 51% of the market, accounting for 5,067 pharmacies.

Medium-sized groups owning six to 99 pharmacies account for 1,706 pharmacies, or 17% of the market. Larger groups owning 100 or more pharmacies account for 3,167 pharmacies, or 32% of the market.

This matters because independent pharmacies are often closer to local patient need, more embedded in their communities and more able to adapt quickly than larger corporate operators. They may also feel financial pressure more sharply, which makes the search for sustainable private services more urgent.

For wellness clinic development, independent community pharmacy is a serious audience. These businesses already have premises, patient trust, clinical capability and local relationships. With the right support, they could be well placed to develop services that meet patient demand while strengthening commercial resilience.

The report shows that the movement towards service-led pharmacy is already happening. Between 2021 and 2025, pharmacy services increased by 300%, rising from 7.5 million to 25 million.

The report also notes a 25% increase in dispensed prescription items over the past decade. Separately, the CCA noted that NHS prescription items dispensed increased by 16% since 2015/16, reaching 1.16 billion in 2024/25.

This matters because pharmacies are being asked to do more, not less. They are handling higher demand while also being encouraged to take on a broader role in patient-facing care.

Looking ahead, 63% of respondents expect expansion in private services. A further 59% anticipate increased dispensing of weight loss medications, 52% predict growth in Pharmacy First, and 45% forecast further increases in dispensing volume.

The opportunity is therefore not to persuade pharmacies that services matter. The report shows the sector is already moving in that direction. The opportunity is to help pharmacies develop services properly, with clear governance, patient safety and commercial logic.

Pharmacy First is one of the clearest examples of the sector’s changing role. Introduced in January 2024, it allows pharmacists to supply prescription-only medicines for seven common conditions: sinusitis, sore throat, earache, infected insect bites, impetigo, shingles and uncomplicated urinary tract infections in women.

Between February 2024 and October 2025, the report states that 4.5 million Pharmacy First consultations were completed, with medicines supplied in 3.5 million cases. By October 2025, participation had expanded to 10,900 pharmacies.

This is a significant shift. It shows community pharmacy moving further into accessible, front-line healthcare. It also shows that patients are already using pharmacies for more than medicine collection.

For CTA, this is relevant because any discussion about pharmacy-based wellness clinics should sit within this wider direction of travel. Pharmacies are becoming more clinical, more service-led and more integrated into patient access pathways.

The report is also clear about workforce pressure. It states that 60% of pharmacy teams are reporting staffing gaps, while 54% of pharmacy owners are struggling to recruit permanent staff.

Patients are already feeling the impact. According to the report, 81% of pharmacy staff report longer waiting times and 57% say they have less capacity to provide advice and services.

This is why any new wellness clinic model has to be designed carefully. It cannot simply be dropped onto an already stretched pharmacy team. It needs proper scheduling, defined roles, patient flow, digital booking, staff training and a realistic understanding of what the pharmacy can safely provide.

A poor clinic model adds pressure. A good clinic model creates structure, protects the team and gives the pharmacy a clearer service offer.

The report also highlights the changing clinical capability of the pharmacy workforce. There are now 67,339 registered pharmacists and 28,274 registered pharmacy technicians across the UK. Of registered pharmacists, 38% have a prescribing annotation, representing 25,866 pharmacists.

The report also notes that 2026 will see the first cohort of newly qualified graduates entering community pharmacy with independent prescribing abilities. In addition, the 2026/27 Community Pharmacy Contractual Framework includes a national NHS independent prescribing offer from autumn 2026.

That offer is expected to sit within Pharmacy First and the Pharmacy Contraception Service, with up to five new prescribing-only pathways expected to be added. The report states that pharmacies delivering the new independent prescribing offer will receive a one-off £500 set-up fee and a £525 monthly infrastructure fee.

This marks a clear direction of travel. Community pharmacy is being positioned as a more clinical part of healthcare, with greater prescribing capability and a stronger role in access to treatment.

A pharmacy-based wellness clinic should not be seen as a gimmick. Done properly, it could help pharmacies use their existing strengths: trust, premises, patient relationships, clinical knowledge and local accessibility.

A wellness clinic model could include pain support, sleep support, weight management, women’s health, menopause services, health checks, medicines optimisation, minor illness support, lifestyle interventions and appropriate referral pathways into specialist services.

Within that wider model, lawful medical cannabis pathways may have a place, but they must be handled carefully. The opportunity is not to rebrand pharmacies as cannabis clinics. The opportunity is to build properly governed wellness clinics where cannabis-related education, support, signposting or dispensing pathways are clearly defined and clinically appropriate.

For many pharmacies, the most sensible model may be partnership. The pharmacy provides local access, trusted patient relationships and a professional healthcare environment. Specialist clinics, doctors or regulated providers deliver the parts of care that require specialist input or oversight.

CTA believes there is an opportunity to support serious pharmacy operators who want to explore wellness clinic models that include lawful medical cannabis pathways responsibly. This is not about pushing cannabis into every pharmacy. It is about helping pharmacies understand where cannabis-based medicines may fit within wider patient care, and where they do not.

The future of community pharmacy is likely to be more clinical, more service-led and more patient-facing. Wellness clinics could become part of that future, but only if they are built properly.

For cannabis, that means one thing above all else: credibility first.

The Pharmacy Show 2026, An Overview of the UK Community Pharmacy Landscape 2026.

https://www.thepharmacyshow.co.uk/download/overview-uk-community-pharmacy-landscape